The Budget 2017 confirmed a number of changes for the new 2017/2018 tax year, which we have detailed below.

Personal Tax

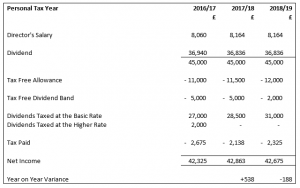

The personal tax free allowance will increase from £11,000 to £11,500 from 6 April 2017. The higher rate income tax threshold will increase from £43,000 to £45,000, meaning you can earn more before paying higher rate tax.

Class 2 and Class 4 National Insurance Contributions are paid by self-employed individuals (this means sole traders, not directors/shareholders of limited companies).

It was previously announced that Class 2 National Insurance Contributions will be abolished from April 2018. In the Budget 2017 Hammond announced that Class 4 National Insurance Contributions will increase from 9% to 10% in April 2018 and 11% in April 2019, however on 15th March it was announced that the Government had decided to scrap these plans for Class 4 National Insurance Contributions.

There was a hit to the tax free dividend allowance which will reduce from £5,000 to £2,000 in April 2018.

An illustration of a director shareholder that takes a director’s salary up to the primary threshold and the remainder of the basic rate band for income tax as dividends is set out below to demonstrate the changes.

Pensions and Savings

The lifetime ISA will come in this April which allows younger adults to save £4,000 each year and receive a bonus of up to £1,000 a year on these contributions, which can be withdrawn tax-free to put towards a first home or when they turn 60.

The present ISA savings limit will rise to £20,000 from April 2017.

The Budget confirms the rate on the NS&I Investment Bond announced at Autumn Statement 2016 will offer a rate of 2.2% over a term of 3 years and will be available for 12 months from April 2017. The Bond will be open to everyone aged 16 and over, subject to a minimum investment limit of £100 and a maximum investment limit of £3,000.

Business Tax

Hammond confirmed that corporation tax rate will be cut to 19% from April 2017 and then cut again to 17% in April 2020.

To support UK investment, the government will make administrative changes to the Research and Development Expenditure Credit to increase the certainty and simplicity around claims and will take action to improve awareness of R&D tax credits among SMEs.

Corporate Property Tax

There will be a business rates revaluation which takes effect in England from April 2017. In addition to the transitional relief which was announced in November 2016, the government will provide £435 million of further support for businesses facing significant increases in bills from the English business rates system.

Other Indirect Taxes

There are changes to the registration and deregistration thresholds for Value Added Tax (VAT). From 1 April 2017 the VAT registration threshold will increase from £83,000 to £85,000 and the deregistration threshold from £81,000 to £83,000.

In respect of Insurance Premium Tax (IPT), the government will legislate to introduce anti-forestalling provisions and increase the standard rate of IPT to 12% from 1 June 2017, as announced at Autumn Statement 2016.

Tax Administration

Hammond announced that the government will provide an extra year, until April 2019, before Making Tax Digital is mandated for unincorporated businesses and landlords with turnover below the VAT threshold. This will provide them with more time to prepare for digital record keeping and quarterly updates. The government will also consult on the design aspects of the tax administration system, including interest and penalties, with the aim of adopting a consistent approach across taxes. This will simplify the system for taxpayers.

The government will increase the cash basis entry threshold to £150,000, and exit threshold to £300,000, and will extend the use of the cash basis to unincorporated landlords.

Other

If you would like to read further into Hammond’s budget, including the areas of UK productivity, public services and markets, financing, budget decisions, government spending and the UK economic outlook the full budget document can be found here.

A Reminder of Previous Changes to Rental Properties That Come in From April 2017

At the moment, landlords can claim tax relief on their mortgage interest payments. In other words, they can offset the cost of the mortgage interest from the rental income when they calculate their profits.

So, if a landlord collects rental income of £10,000 a year, but pays mortgage interest of £9,000, the profit is the difference between the two, or £1,000.

Landlords pay tax on their profits according to their income tax band. So, in this simplified example, a basic-rate taxpayer would pay 20% tax on £1,000, or £200, and keep £800.

The tax bill for a 40% taxpayer would be £400, leaving £600, or £450 for a taxpayer at the 45% additional rate, leaving £550.

However, mortgage interest tax relief will gradually be cut back to 20% between 2017 and 2020.

So, a landlord with rental income of £10,000 and £9,000 of mortgage interest to pay will in future have to pay tax on the full amount, less a 20% credit on the mortgage interest.

The tax bill for a higher rate taxpayer would therefore work out at £4,000 (40% of £10,000 profit) minus £1,800 (20% of £9,000 interest), which equals £2,200, up from £400 under the current tax regime.

That’s a significant increase of £1,800. A landlord who pays 45% tax could expect a tax bill of £2,700, compared with £450.

The tax liability of a basic-rate taxpayer is unchanged. However, the new profit calculation could push a basic-rate taxpayer into a higher tax band.

Article written by ICS Head of Finance, Maggie Aston-Green

Winner")