The chancellor, Philip Hammond, has delivered the budget for the tax year commencing April 2019 and beyond. We have set out the key areas that will impact you, as a limited company contractor, from the 2018 Budget.

IR35 Off Payroll Working in the Private Sector

The chancellor has announced that the private sector reform of IR35 will take place in April 2020. As it stands, it is the contractor’s responsibility to determine whether they are operating inside (also known as caught by) IR35 or outside IR35. If the contractor makes the wrong determination then their personal service company is liable for any unpaid taxes.

From April 2020, medium and large businesses will need to decide whether the rules apply to an engagement with individuals who work through their own company. Where it is determined that the rules do apply, the business, agency, or other third party paying the worker’s company will need to deduct income tax and employees National Insurance Contributions and pay employer National Insurance Contributions.

This means that from 2020 your end client will have to undertake an IR35 assessment for each assignment you undertake with them and decide whether you are operating inside or outside IR35. ICS Accounting are able to undertake contract reviews as well as looking at how it interacts with your working practices in an effort to mitigate IR35 risk.

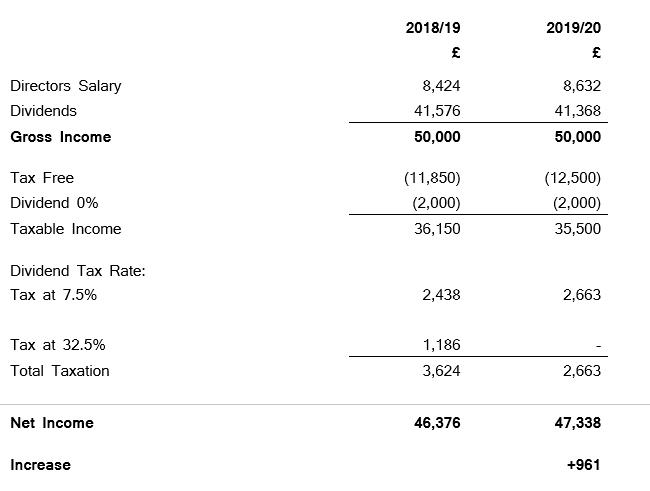

Personal Tax

The tax free allowance will increase to £12,500. In addition, the higher rate threshold will increase to £50,000.

This is an overview of what this looks like from the perspective of fully utilising your basic rate income tax band.

Entrepreneurs Relief

A valuable relief available to business owners selling, or closing their business: Entrepreneur’s relief, was protected, but the qualifying condition of 12 months ownership before eligibility was doubled, to 24 months.

Pensions and Savings

The pension annual allowance will remain at £40,000 with the potential to bring forward unused allowances for the previous three tax years. The allowance is tapered where total income exceeds £150,000.

There were no ISA announcements in the budget so we therefore expect the overall limit to remain at £20,000 which can be used across:

- Cash ISAs

- Stocks and shares ISAs

- Innovative finance ISAs

- Lifetime ISAs

Business Tax

The Chancellor has confirmed that the corporation tax rate will remain unchanged from the previous Budget, staying at 19% at present and changing to 17% from 2020.

Other Indirect Taxes

It was confirmed that the VAT threshold will remain the same at £85,000 until 2020. This is a welcome announcement given in the introduction of Making Tax Digital in April 2019 which will require every business with a turnover above the VAT threshold to file their information electronically, in a prescribed format, with HMRC at least once per quarter.

Rental Properties

A gain made on selling a residential property is subject to CGT at 18% (basic rate) or 28% (higher rate unless the property, as their main home, is exempt. This is called principle private residence relief – PPR relief. Two specific aspects have come up in the budget as set out below.

Lettings relief

If the property has been let out at any point, each owner can claim a relief which reduces the gain subject to tax. The relief is a maximum of £40,000 but is only available where the property has been their main home at some point. The government is proposing to restrict lettings relief to cover only periods in which the owner is also occupying the same property at the same time from 2020.

Last few months

In addition, there is a potential relief where the homeowner vacates the property before it is sold. When calculating capital gains tax there is a period of deemed occupancy meaning capital gains tax does not arise on that portion of the gain. Currently this period is 18 months however the chancellor accounted that this will reduce to just 9 months from 2020.

Further Information

If you would like to read further into Hammond’s budget, including the areas of UK productivity, public services and markets, financing, Brexit, government spending and the UK economic outlook the full budget document can be found here.

If you have any questions on the above or accounting and taxation in general, please do not hesitate to get in touch on 0800 195 3750 or email info@icsuk.com