What has changed?

Until April 2020 it is the contractor’s responsibility to determine whether they are operating inside (also known as caught by) IR35 or outside IR35. If the contractor makes the wrong determination then their personal service company is liable for any unpaid taxes.

With the introduction of the new legislation from 5 April 2020 the responsibility, and therefore any potential tax liabilities, falls with the engager if they are medium or large. The company paying your personal service company will be liable for the Income Tax and National Insurance that becomes payable if the role is considered inside IR35, it will receive confirmation from the end client who will have a legal responsibility to provide that opinion for the role. In the majority of cases the company paying your personal service company will be a recruitment agency.

This means that moving forward, if your end client is medium or large, it will have to undertake an IR35 assessment for each assignment you undertake with them and decide whether you are operating inside or outside IR35.

Who will it impact?

The changes apply to those working through a limited company. They do not apply to the self employed.

From 6 April 2020, medium and large businesses will need to decide whether the rules apply to an engagement with individuals who work through their own company.

What will the impact be?

If your client’s assessment is that the assignment is outside IR35 then the director/shareholder can continue to extract profits in a combination of salary and dividends.

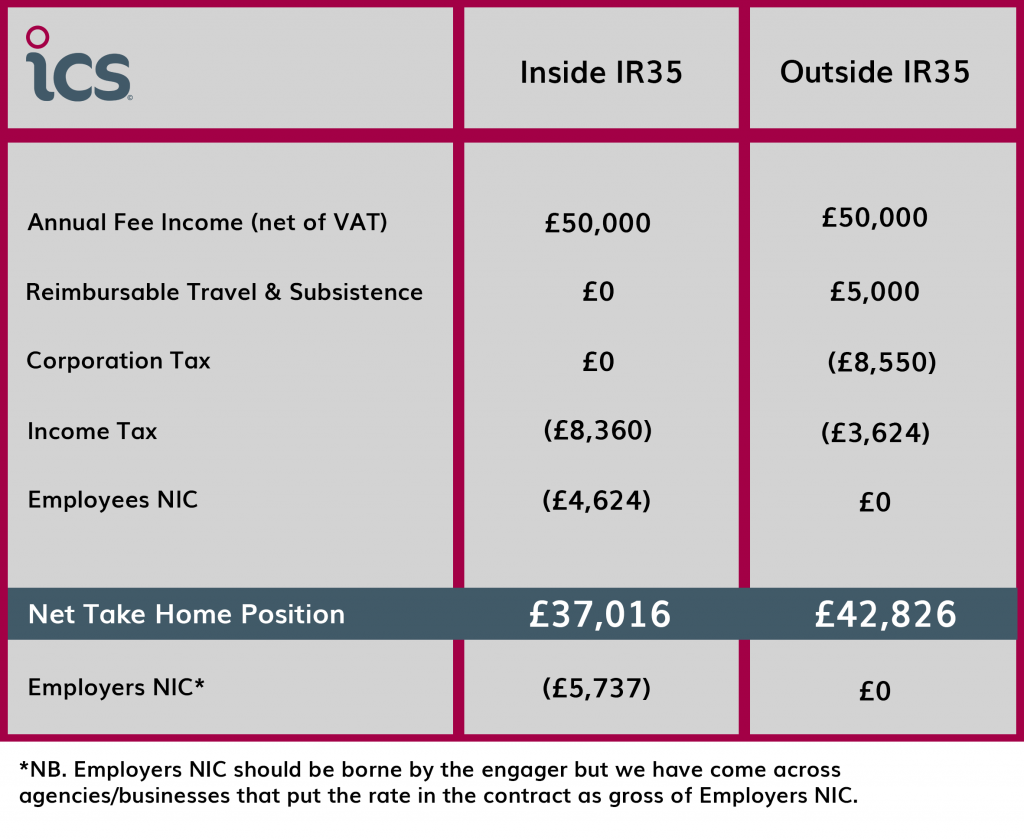

If your client’s assessment is that the assignment is inside IR35 all of the fees will be subject to income tax and national insurance. A comparison is set out below:

When will the legislation be published?

A further consultation on the detailed operation of the reform will be published in the coming months. This consultation will inform the draft Finance Bill legislation, which is expected to be published in Summer 2019.

What will my options be going forward?

The final legislation has not been released and therefore your agency/end client probably haven’t taken any steps to assess your IR35 status.

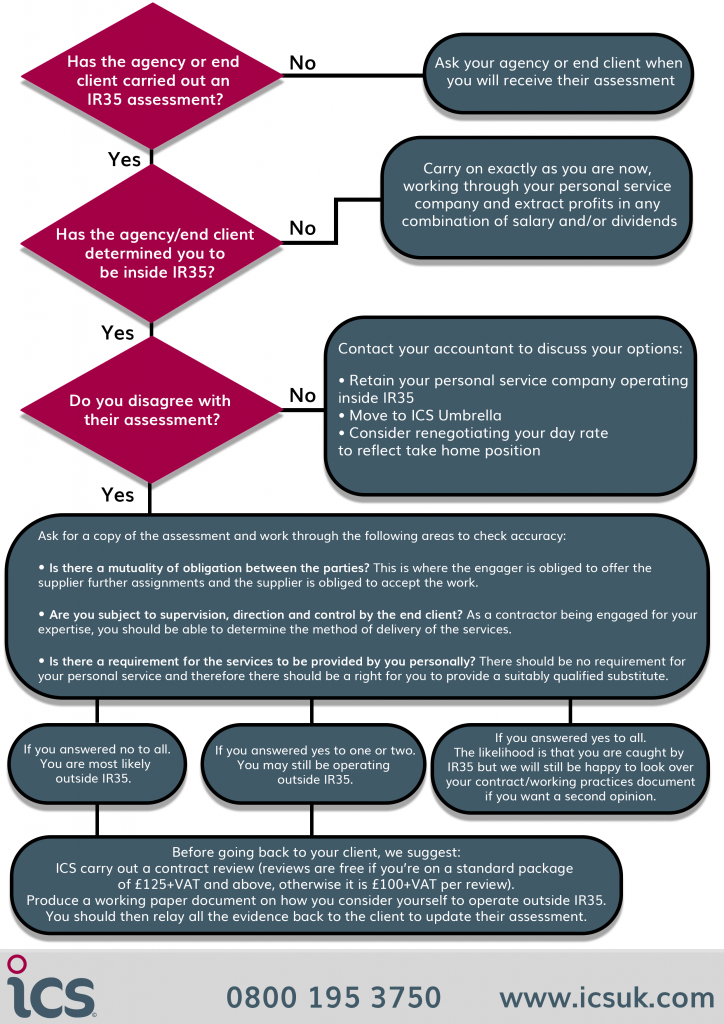

If your client has started their assessment on you then you can follow through our decision tree to work out what your next steps should be:

For more information on how ICS can help you, call for free on 0800 195 3750 or email info@icsuk.com