We are exactly a fortnight away from a new year – tax year that is.

It might not all be fireworks and parties, but a new tax year can be something to celebrate, particularly when you keep more money in your pocket.

The tax year runs from 6th April to 5th April.

A small amount of planning can ensure that you fully utilise all the tax opportunities that exist.

Max Out Your Basic Rate Tax Allowance – Use It or Lose It

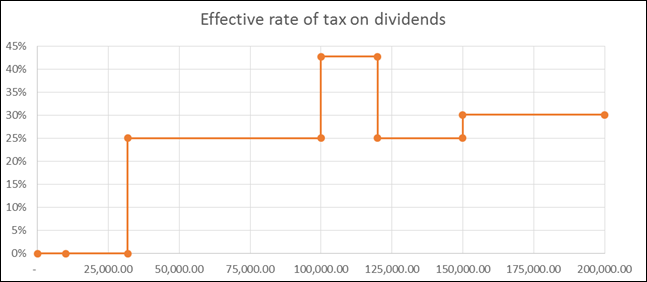

Ensure you draw any available dividends from your company that will take your total income up to the higher rate threshold – where they are tax-free! For 2014/15, that is £41,865.

Keep Your Income Below £50,000 – Hang Onto Child Benefit

Parents can receive Child Benefit of £20.50 per week for the first child, with £13.55 for each additional child. Unfortunately, this benefit is clawed back if either parent’s income exceeds £50,000. For each £100 earned over this mark, 1% of the benefit received is clawed back through the tax return.

Keep Your Income Below £100,000 – Avoid a 47.2% Effective Tax Rate

At £100,000, the entitlement to the annual allowance of £10,000 starts to erode. The tax-free allowance is reduced by £1, for each £2 earned in excess of that threshold.

Keep Your Income Below £150,000 – Don’t be an Additional Rate Payer

For those fortunate enough to earn in excess of £150,000, the additional rate tax kicks in, which on dividends attracts an effective rate of 30.1%.

Spouse Shareholding – Husband and Wife Pay Tax at Different Rates

The aforementioned planning focusses on the restriction or maximisation of dividends to a specific level. An alternative to this approach which can help to maintain a high level of dividends can be to transfer a percentage of company shares to a spouse. This would entitle the owner to dividends. If the partner has income in a lower income bracket, this can be utilised, perhaps receiving income and paying tax at 0% rather than the spouse suffering 25%, or keeping the partner under the additional rate threshold, even if they are themselves a higher rate payer.

Pension Contributions – Top Up Your Pot and Save Tax

Pension contributions made personally to your scheme are deducted in calculating your net income. This is important when assessing whether the entitlement to personal allowance (£100,000) or child benefit (£50,000). A contribution when income slightly exceeds those levels can be useful.

Donations – Do Your Bit and Keep Your Tax Bill Down

In the same way as above, donations to charities are deducted from income when considering if income exceeds thresholds for losing personal allowance and child benefit.

Article written by Sam Price, ACA IIT(DIP) MAAT from ICS. Sam is a Chartered Accountant and tax adviser who specialises in helping our contractors prosper. He achieves this through a proactive and bespoke approach to each client. He has worked across tax, accounts and audit departments in accountancy practices and in industry.

This article is for guidance purposes only. For more detailed information, please contact Sam Price at ICS for a bespoke approach to your tax affairs or alternatively speak to your qualified accountant.